Financial review

Following the overview of our 2025 developments in the Delivery 2025 chapter, this section presents our performance on the financial key performance indicators (KPIs) applicable for 2025. These KPIs reflect how we delivered on our strategy across our financial priorities. For more information on the financial KPIs, see the financial statements.

Our new KPIs, introduced at the Capital Markets Day in September 2025 and applicable from reporting year 2026, are explained on page .

Revenue and normalised EBIT

PostNL applies three KPIs, revenue, normalised EBIT and free cash flow, in its management analyses and reports on financial performance. Normalised EBIT gives a reflection of the operating income performance, adjusted for the impact of project costs and incidentals. Free cash flow gives a reflection of the ability to generate cash available for dividend distributions, acquisitions, and/or debt repayments.

Normalised EBIT and free cash flow represent non-GAAP financial measures and should not be viewed in isolation as alternatives to the equivalent IFRS measures, which are presented in the consolidated financial statements, but should be used in conjunction with the most directly comparable IFRS measures. Non-GAAP financial measures do not have a standardised meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers.

PostNL Business performance in € million

Volume | Revenue | Normalised EBIT1 | |||||

|---|---|---|---|---|---|---|---|

Year ended at 31 December | 2024 | 2025 | 2024 | 2025 | 2024 | 2025 | |

Parcels2 | 371 | 376 | 2,393 | 2,457 | 65 | 61 | |

Mail in the Netherlands2 | 1,605 | 1,529 | 1,313 | 1,315 | 3 | 2 | |

PostNL Other | 240 | 251 | (16) | (10) | |||

Intercompany | (694) | (699) | |||||

PostNL | 3,252 | 3,324 | 53 | 53 | |||

| 1 | Normalised figures exclude one-off items of €42 million in 2025 and €15 million in 2024. | ||||||

| 2 | As from 1 January 2025, all activities and organisational responsibilities related to real estate are reported at Parcels (until 31 December 2024 at Mail in the Netherlands). The comparative figures have been adjusted accordingly. | ||||||

Normalised EBIT excludes exceptional items, which amounted to €(42) million in 2025 (2024: €(15) million), mainly due to a goodwill impairment of €40 million in Mail in the Netherlands. Further information on the bridge from operating income to normalised EBIT can be found in note 2.7 Segment information to the Consolidated financial statements.

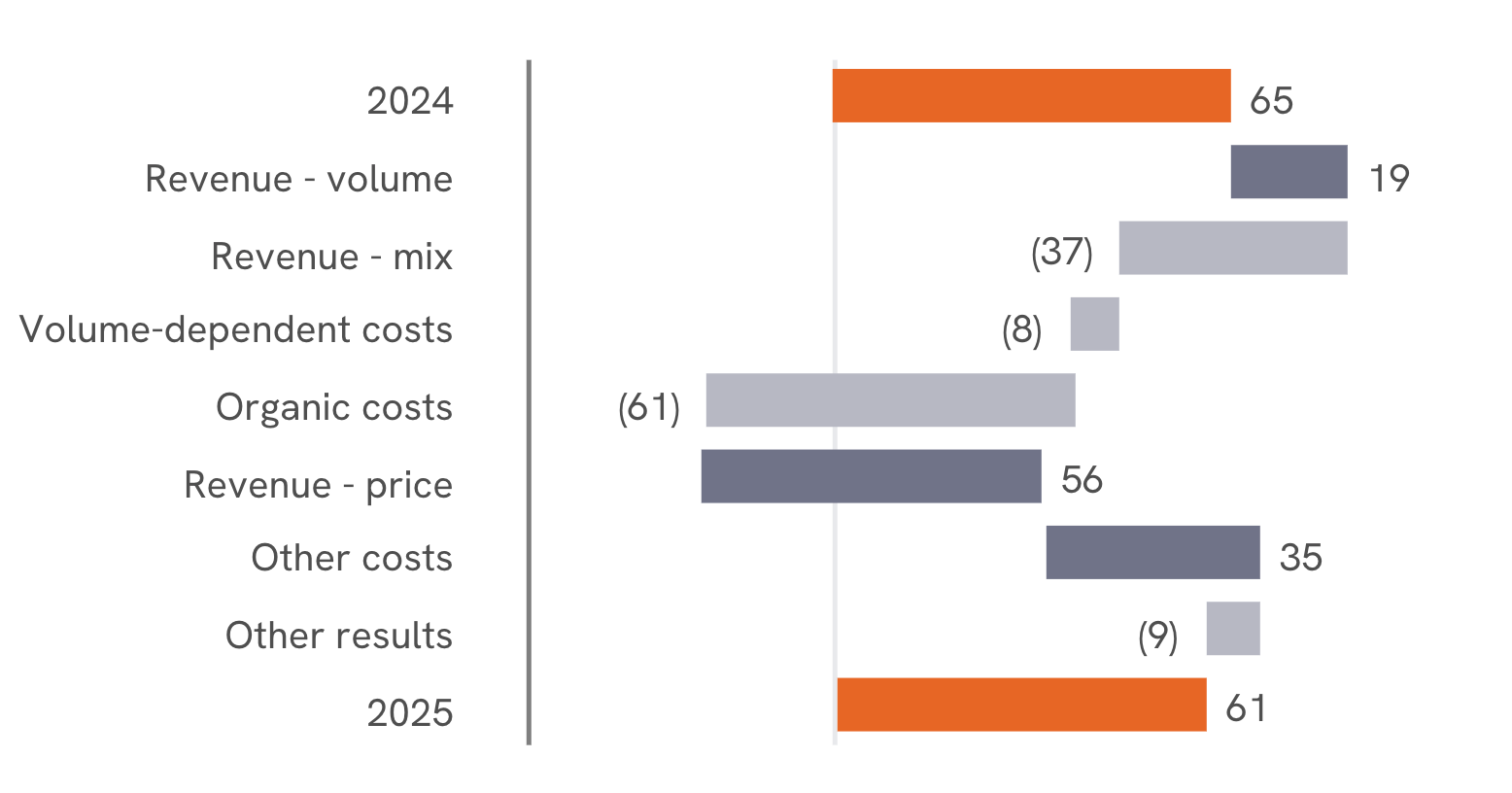

Parcels

In 2025, we delivered 376 million parcels (2024: 371 million). This resulted in a 1.2% volume growth compared to 2024.

Revenue grew to €2,457 million (2024: €2,393 million) driven by volume growth and price increases, while the shift in product and customer mix was unfavourable. Revenue at Spring was up, mainly driven by our intra-European activities.

Normalised EBIT decreased by €5 million, from €65 million in 2024 to €61 million in 2025.

Normalised EBIT Parcels in € million

Organic costs increased by €61 million due to higher wage costs following collective labour agreement increases and indexation in contracts with delivery partners. Other costs decreased by €35 million, mainly caused by efficiency improvements.

Other results decreased by €9 million, primarily due to mix effects at Spring and the impact of investments in expanding international growth.

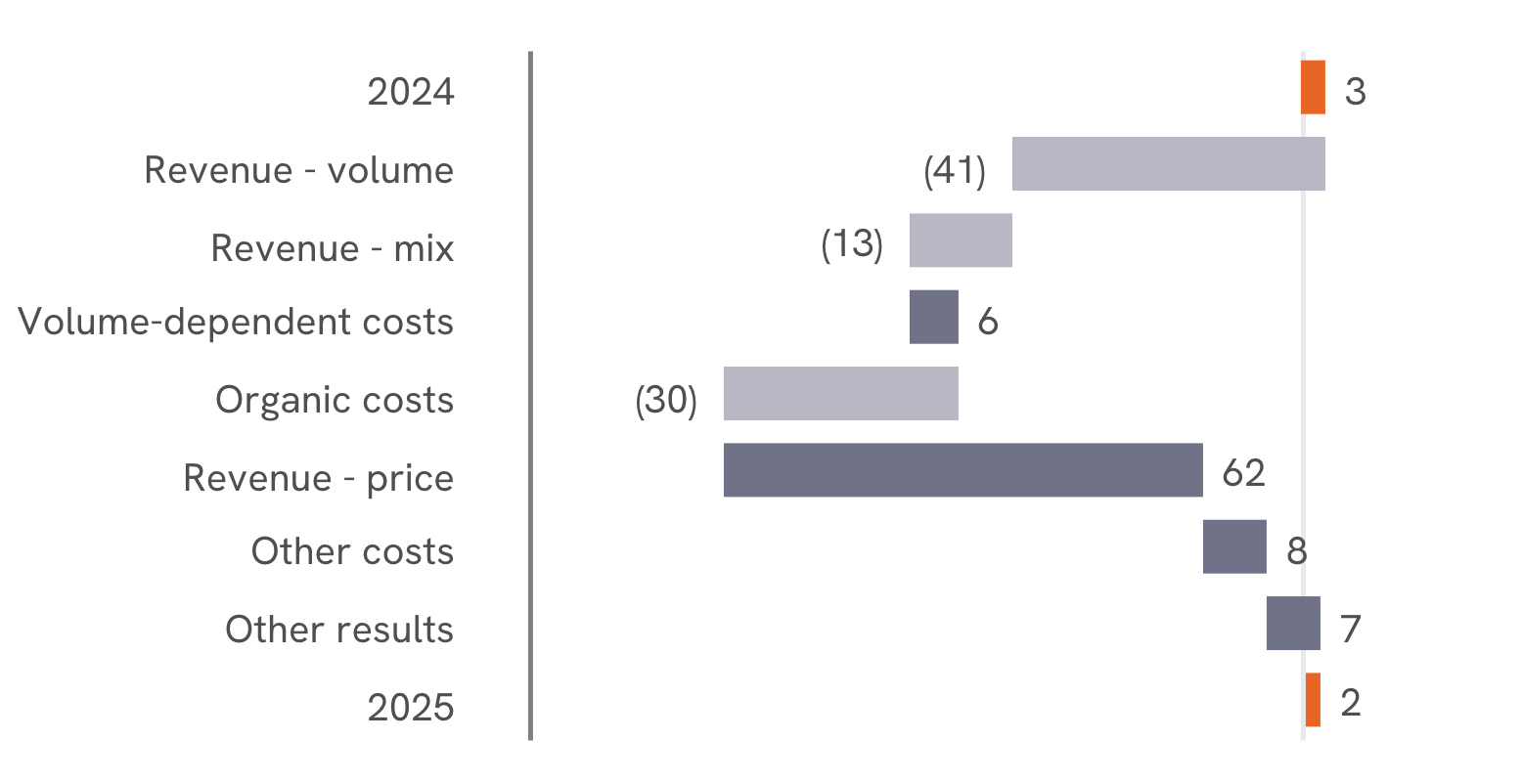

Mail in the Netherlands

In 2025, we delivered 1,529 million mail items (2024: 1,605 million items). This resulted in a reported volume decline of 4.8% compared to 2024, mainly due to ongoing substitution. Volume development in the year was supported by election mail and some large non-recurring mailings, for example from pension funds.

Revenue at Mail in the Netherlands increased slightly to €1,315 million (2024: €1,313 million). The volume decline, combined with a negative mix effect due to a shift in products, was more than offset by price increases, resulting in a total positive impact of €8 million on the revenue of Mail in the Netherlands.

Normalised EBIT Mail in the Netherlands in € million

Normalised EBIT decreased by €1 million, from €3 million in 2024 to €2 million in 2025.

Organic costs increased by €30 million mainly due to collective labour agreement increases and inflation.

Other costs decreased by €8 million, as cost savings of €37 million were partly offset by a lower result on bilaterals and several other, partly non-recurring, effects. Other results were up €7 million, mainly explained by international mail.

PostNL's position on the Future of Mail in the Netherlands can be found on the Our vision for a future-proof postal service page in the Delivery in 2025 chapter.

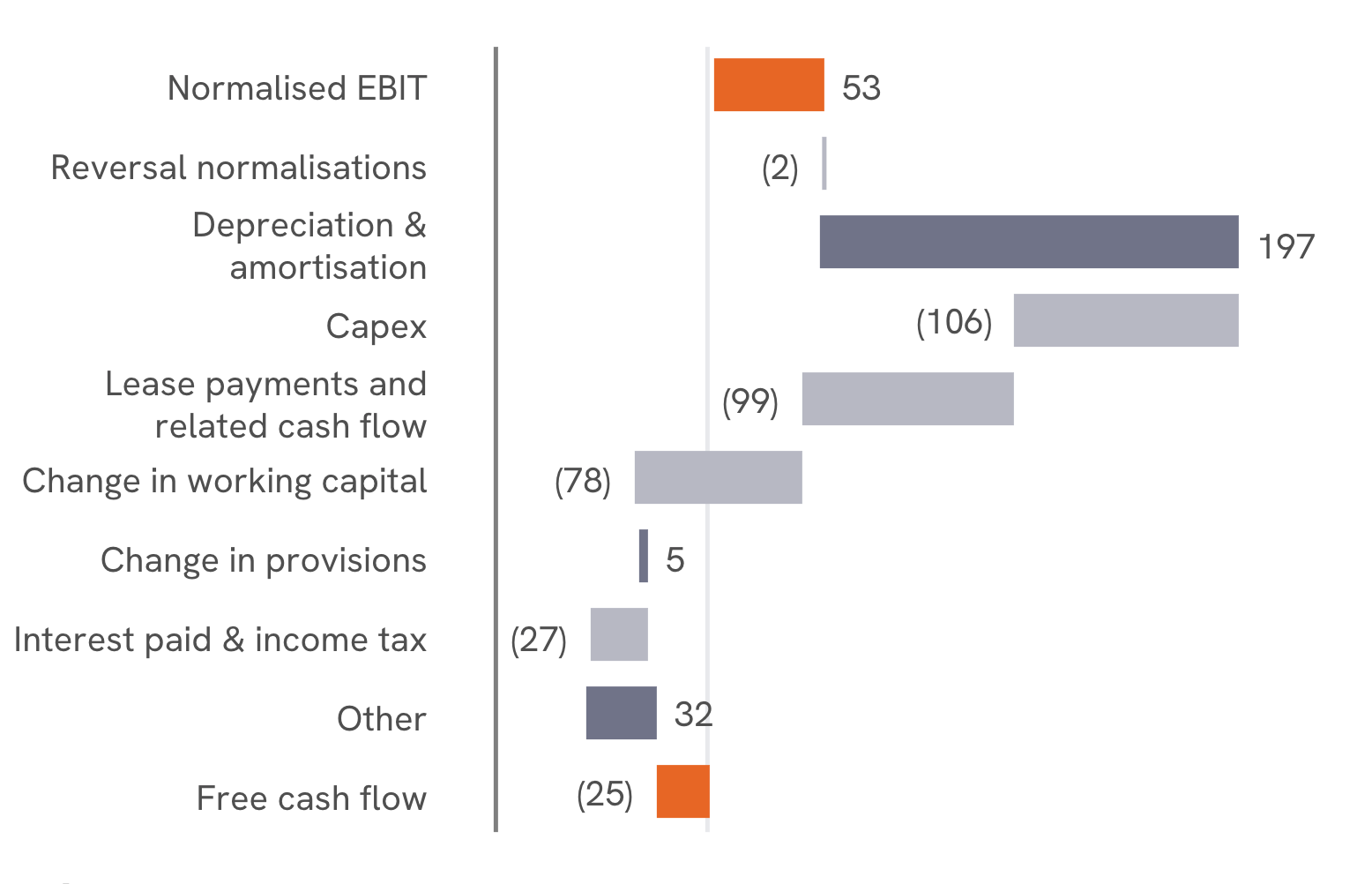

Free cash flow

Free cash flow in € million

2025

1Excluding goodwill impairment Mail in the Netherlands of €40 million

We prioritise capital allocation based on a sound financial framework, taking into account developments in our results, return on invested capital (ROIC) and cash conversion, to fund further growth and provide sustainable shareholder returns.

Throughout the year we continued to invest in our business and digital transformation, health and safety measures and automated parcel locker (APL) network to strengthen our competitive position. The strong focus on capex as well as strict working capital management contributed to the cash flow performance. The negative change in working capital mainly reflects phasing effects from previous year. The negative free cash flow performance in 2025 was in line with expectations.

Free cash flow is defined as cash flow before dividend, acquisitions, redemptions of bonds and other financing activities, and after payment of leases. The repayment of leases and related cash flows, reported as cash used in financing activities following the adoption of IFRS 16, are as such included in our calculation of free cash flow.

Return on invested capital

Our aim is to generate a positive spread of the ROIC over the post-tax WACC. PostNL defines ROIC as net operating profit less adjusted tax (NOPLAT) divided by invested capital. For 2025, the ROIC for the Group was 4.7% (2024: 3.4%). The increase of the ROIC compared to 2024 is explained by an increase in NOPLAT. Invested capital was stable at €804 million compared to 2024. Higher investments in working capital were offset by lower goodwill following the goodwill impairment at Mail in the Netherlands.

PostNL Return on invested capital in € million, unless indicated otherwise

Year ended at 31 December | 2024 | 2025 | |

|---|---|---|---|

Operating income1 | 37 | 51 | |

Less adjusted tax | (10) | (13) | |

Net operating profit less adjusted tax (NOPLAT) | 28 | 37 | |

Property, plant and equipment | 467 | 449 | |

Intangible fixed assets (incl. goodwill) | 414 | 372 | |

Right-of-use assets | 281 | 289 | |

Current assets/liabilities2 | (255) | (217) | |

Other items | (102) | (89) | |

Invested capital | 804 | 804 | |

Return on invested capital (ROIC) | 3.4% | 4.7% | |

| 1 | 2025, excluding goodwill impairment Mail in the Netherlands of €40 million | ||

| 2 | As of 2025, only the assessed minimum operational cash needed is included in the calculation of invested capital. The comparative figures have been adjusted accordingly. | ||

Adjusted net debt

At 31 December 2025, adjusted net debt amounted to €501 million (2024: €474 million). See note 4.1 Adjusted net debt to the Consolidated financial statements for more information and the breakdown of adjusted net debt.

In June 2025, PostNL completed a Schuldschein transaction, securing €100 million in funding. In September 2025, a €300 million bond was issued with a term of five years and an annual coupon of 4.000%. The proceeds will be used for general corporate purposes, including refinancing. The bond transaction marks a next step in aligning our funding with our Breakthrough 2028 ambition, which aims to drive PostNL towards a future of sustainable growth and innovation. Additionally, PostNL repurchased €195 million of the outstanding 0.625% eurobond maturing in September 2026.

Leverage ratio

The leverage ratio, being adjusted net debt divided by adjusted EBITDA, slightly increased from 1.95 in 2024 to 1.99 in 2025 and is in line with our ambition to be properly financed.

PostNL Leverage ratio in € million, unless indicated otherwise

Year ended at 31 December | 2024 | 2025 |

|---|---|---|

Adjusted net debt | 474 | 501 |

Operating income | 37 | 11 |

Depreciation, amortisation and impairments | 188 | 237 |

Proxy for short-term leases and leases of low-value assets | 4 | 4 |

Normalisations on EBIT | 15 | 42 |

Reversal of normalised depreciation, amortisation and impairments | (2) | (42) |

Adjusted EBITDA | 243 | 252 |

Leverage ratio | 1.95 | 1.99 |

Normalised comprehensive income

In 2025, PostNL's normalised comprehensive income amounted to €21 million (2024: €38 million). The decrease mainly relates to higher net financial expenses (€20 million) due to interest expenses from new Schuldschein loans and eurobonds, interest on taxes and lower interest income from cash and short-term investments.

PostNL Normalised comprehensive income in € million

Year ended at 31 December | 2024 | 2025 |

|---|---|---|

Profit/(loss) for the year | 18 | (17) |

Other comprehensive income | 8 | 3 |

Comprehensive income | 26 | (14) |

Normalisations on EBIT (less statutory tax) | 11 | 37 |

Normalise result from discontinued operations | 1 | (1) |

Normalised comprehensive income | 38 | 21 |

Dividend

Our Dividend Policy states that dividend distribution is conditional on being properly financed in accordance with our financial framework. PostNL is steering for a solid balance sheet with a positive consolidated equity, aiming at a leverage ratio not exceeding 2.0 and applying strict cash flow management. This condition was met at the end of 2025. As a result, PostNL will recommend to the Annual General Meeting of Shareholders, to be held on 14 April 2026, a pay-out of 80% of normalised comprehensive income for 2025. This results in a proposed dividend of €0.04 per ordinary share (2024: €0.07). Since no interim dividend was distributed, the full amount will be paid as a final dividend in May 2026.

Outlook

2026 will be fully dedicated to the execution of the new strategy. This year, PostNL expects to reach the inflection point in the trajectory towards delivering on its Breakthrough 2028 ambition.

Our outlook for 2026 is:

PostNL Outlook in € million

| Year ended at 31 December | 2025 | 2026 outlook |

|---|---|---|

Normalised EBIT | 53 | 40 - 70 |

Free cash flow | (25) | 0 - (30) |

Revenue is expected to grow between 5% and 7% in 2026 (2025: €3,324m). Overall, targeted yield measures will gain traction with significant price increases expected to more than offset organic cost increases (~€140 million).

In 2026, PostNL will invest in its strategic initiatives, resulting in a step-up in capex to around €125 million (2025: €106 million), while lease payments will be around the same level as last year (2025: €99 million).

The outlook for 2026 assumes limited impact from changes in treatment of de minimis thresholds in the EU and US, or in related customs handling and clearance fee structures. The scope and timing of these developments could evolve during the year and could impact performance.

Main assumptions per segment

At E-commerce, PostNL assumes volume growth of 1%-3% while maintaining its strong market position. Targeted yield measures come into effect gradually and materially contribute to the performance. Furthermore, the focus on strict cost control is expected to bring between €40 million and €50 million in cost savings. As of mid 2026, letterbox parcels (D+1) will be transferred from the Mail infrastructure to the delivery network of E-commerce. The related volumes are not included in the aforementioned volume assumption. The transition has limited impact on normalised EBIT in 2026 due to transition costs and is expected to be margin accretive as of 2027.

At Platforms, PostNL will accelerate its plans to strengthen its position in intra-European logistics (Spring and MyParcel) and broaden its Asian base beyond China. The main drivers for the 2026 performance are an assumed double digit revenue growth, while at the same time PostNL will continue to invest in further expansion of its international activities.

At Mail, PostNL assumes a volume decline of between 8% and 10%. Price increases are expected to offset organic cost increases and part of the volume decline. In line with the roadmap towards a future-proof postal service, PostNL expects to achieve between €30 million and €40 million in cost savings, which will be more than offset by additional costs for letterbox parcels and higher other costs, related to future-proof postal network. The transfer of letterbox parcels (D+1) to the E-commerce network is a necessary step to enable the transition to D+3 in 2027.