2.5 EU Taxonomy on sustainable activities

Since 2021, the EU Taxonomy on sustainable economic activities applies to PostNL. The EU Taxonomy is the EU's dictionary of sustainable economic activities designed to promote transparency, counter greenwashing, and drive the shift of capital towards a future sustainable economy. In this chapter, PostNL provides the mandatory disclosures required.

The Taxonomy is a classification system for companies to disclose the extent to which business activities are covered by and aligned with specific sustainability criteria. The main objectives of the EU taxonomy are to provide a reference framework aimed at orienting financial and business investment strategies towards sustainable activities and to accelerate the green and sustainable transition of economic players. Reaching these objectives is essential to meet the EU's ambition of becoming climate neutral by 2050.

2.5.1 EU Taxonomy statements

This chapter contains an elaboration of the assessment on the classification of eligible and aligned activities in accordance with the EU Taxonomy. Given the evolving nature of legislation, our eligibility and alignment assessments follow an iterative approach. These efforts lay the groundwork for future EU Taxonomy implementation and reporting.

The EU Taxonomy prescribes quantitative and qualitative reporting on predefined KPIs. In this section, we present the share of PostNL’s consolidated total revenue (turnover), capital expenditure (capex) and operational expenditure (opex) for the reporting period 2025. The disclosures are associated with Taxonomy-eligible economic activities related to the environmental objectives in accordance with the Regulation (EU) 2020/852 as supplemented with Commission Delegated Regulation (EU) 2021/2139, Commission Delegated Regulation (EU) 2021/2178 (EU Taxonomy), Delegated Regulation (EU) 2023/2486 of 27 June 2023 (Environmental Delegated Act) and the Delegated Regulation (EU) 2023/2485 of 27 June 2023 amending the Climate Delegated Act. In line with the option provided by the legislation, PostNL has chosen to apply, starting from this reporting year, the requirements set out in the Delegated Act amending the Taxonomy Disclosures as well as the Climate and Environmental Delegated Acts (Commission Delegated Regulation (EU) 2026/73 of 4 July 2025).

Basis of preparation

Our approach to report in accordance with the relevant EU Taxonomy regulation includes the following key steps:

- Evaluation of PostNL's activities in relation to the EU Taxonomy classification of economic activities

- Evaluation of technical specifications of activities and related assets in relation to substantial contribution and Do No Significant Harm (DNSH) criteria

- Evaluation of Minimum Safeguards (MS) criteria based on existing policies and business practices

- Materiality assessment and decision-making on whether or not to apply the threshold (10%) per activity and KPI

- Calculation and reporting of the KPIs.

Identification of economic activities

An economic activity is considered Taxonomy eligible if it is described in the Taxonomy Delegated Acts, irrespective of whether that activity meets any or all of the technical screening criteria laid down in the Delegated Acts. An economic activity is considered Taxonomy aligned when the activity contributes substantially to one of the six environmental objectives, DNSH to the other five objectives in accordance with the DNSH criteria, and complies with Minimum Safeguards.

Assessment of technical screening criteria

In 2021 and 2022, the technical screening criteria for substantial contribution was specified by the EU for environmental objectives:

- Climate change mitigation (CCM)

- Climate change adaptation (CCA)

- Sustainable use and protection of water and marine resources

- Transition to a circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems.

These criteria relate to how an economic activity can contribute substantially to one or more of the environmental objectives, in combination with criteria for DNSH to the other environmental objectives. The 2025 Delegated Act amending the Taxonomy Disclosures introduced a change in the Appendix C related to the DNSH criteria for pollution prevention and control, however this is not applicable to PostNL’s eligible activities.

In assessing the technical screening criteria, PostNL incorporates the 2025 update of the Climate Risk Assessment. Further information on this assessment can be found in the strategy section earlier in the Environmental disclosures.

Minimum safeguards

PostNL has assessed its compliance on the minimum social safeguards the EU Taxonomy requires in relation to human rights, anti-bribery, fair competition and taxation matters, taking into account the 2025 Human Rights Salience Assessment. Further information on this assessment is provided in the strategy section of the Social disclosures. PostNL has included relevant aspects of business conduct in relation to these topics in formal policies and procedures as part of our business conduct and integrity programme. The assessment provided PostNL a sufficient basis to conclude that the company met the minimum social safeguards criteria. More details about business conduct and integrity in general can be found in the Governance disclosures.

EU Taxonomy KPIs

For 2025, PostNL reported on the KPIs total revenue (turnover), capital expenditures (capex) and operational expenditures (opex). The starting points of our Taxonomy allocation methodology are the financial statement line items. The reported figures have been determined based on the allocation of activities to the Taxonomy, derived bottom-up for all PostNL reporting units. The figures are based on the actual amounts represented in the general ledger accounts as included in PostNL's consolidated financial statements. In addition, the split between transport by road and air in our international business is based on expected transport modes between countries for our trade lanes. Only the road activities are eligible for PostNL, transport by air is considered to be a non-eligible activity for PostNL. To avoid double-counting, we eliminated inter-company transactions, which are separately specified in our general ledger accounts and consolidated financial statements. We did not identify any other risk of overlapping activities that could lead to double-counting.

Significant estimates and judgements

PostNL has implemented the Taxonomy-related requirements based on the detailed regulatory documents, frequently asked questions (FAQs) from the European Commission and, where needed, our own interpretation of the criteria. On relevant elements where interpretation is needed, PostNL applied due care in its approach by focusing on maximum transparency and through engagement with dedicated professional consultants and peers, for example a PostEurop working group. We are aware that views on the interpretation by the European Commission may change over time and that this may lead to different conclusions on the reported eligibility and alignment in the future. For CCM 6.4 (Operation of personal mobility devices, cycle logistics) and CCM 6.5 (Transport by motorbikes, passenger cars and light commercial vehicles), the calculation of the share of aligned activities, PostNL allocated the proportion of turnover based on the kilometres driven by the Taxonomy-aligned activities relative to the total kilometres driven by vehicles attributed to this economic activity.

The share of Taxonomy-aligned activities for CCM 6.5 is currently built up from electric scooters. For small e-trucks in our fleet, we concluded that these cannot yet be reported as Taxonomy aligned, because PostNL has not yet been able to substantiate the DNSH criteria for the environmental objective Pollution. All other technical screening criteria are being met for the activities with these vehicles.

2.5.2 Methodology and assumptions

PostNL has identified the following EU Taxonomy economic activities and key interpretation elements.

CCM 6.4 Operation of personal mobility devices, cycle logistics

All transport devices where the propulsion comes from the physical activity of the user, from a zero-emissions motor and combined with physical activity, such as an (e-)bike and/or (electric) cargo bike (i.e. bicycles, electric bicycles, or cargo bikes) are categorised under activity 6.4. This means that the kilometres of the delivery process, using a personal mobility device such as an (e-)bike and/or (electric) cargo bike, in combination with physical activities (kilometres walked by our delivery staff), are categorised under activity 6.4.

CCM 6.5 Transport by motorbike, passenger car and light commercial vehicle

The purchase, financing, renting, leasing and operation of vehicles designated as category M1, N1, or L (2- and 3-wheel vehicles and quadricycles). In PostNL terminology, all activities with small trucks, motorised scooter and light electric freight vehicles are attributed to this category.

CCM 6.6 Freight transport services by road

This activity concerns power-driven vehicles having at least four wheels and which are used for the carriage of goods. In PostNL terminology, the activities with large trucks are attributed to this economic activity.

CCM 6.15 Infrastructure enabling low-carbon road transport and public transport

PostNL links its sorting activities to a specific sub-activity described in the EU Taxonomy, infrastructure dedicated to transshipment. Our interpretation of this activity is that infrastructure and related activities in the sorting centres of PostNL are related to transshipment of freight between the modes (Delegated act Annex 1 art. 6.15: 1.b of the technical screening criteria).

Capex related to buildings are considered eligible under CCM 6.15. This infrastructure facilitates cargo transition between road freight and other transport modes and is fundamental to enable the efficient transport of letters and parcels. The infrastructure between the modes is therefore indispensable to minimise the required transport activities in our business. Other alternatives would imply a significant expansion of transport movements and related environmental impact, resulting in increased GHG emissions.

Other eligible but non-material activities

According to the Commission Delegated Regulation (EU) 2026/73 of 4 July 2025, undertakings are not required to assess compliance with the EU Taxonomy for activities that are not financially material to their business. Such immateriality is presumed when the cumulative value of these activities represents less than 10% of the KPI denominators.

PostNL rents and leases buildings on a limited scale for operational purposes. This can be considered as “exercising ownership of real estate,” which falls under the economic activity CCM 7.7 “Acquisition and Ownership of Buildings”. As shown in Template I, column 14, this activity accounts (rounded) for 0% of PostNL’s Revenue and 0% of PostNL’s capex denominator and has therefore been classified as non-material in accordance with EU Taxonomy guidance; in the absence of the materiality exemption, this activity was disclosed in the sustainability statements of previous years, since eligible but not aligned.

Operational Expenditure (opex) are not material for PostNL's business model

PostNL is a people-driven, asset-light company where operational expenditure, as defined by the EU Taxonomy, are considered immaterial to the business model. In such cases, the EU Taxonomy permits a reporting exemption (Article 8 Delegated Act, Annex I, Section 1.1.3.2).

To ensure transparency and consistency, PostNL annually assesses this immateriality by comparing the share of opex in scope of the EU Taxonomy to total opex against an internally defined threshold of 5%. If immateriality is confirmed, PostNL reports the opex KPI in accordance with the Disclosure Delegated Act, setting the numerator to zero and disclosing the total opex denominator. For FY2025, PostNL’s opex remains below the defined threshold. Accordingly, this information is presented in the dedicated table.

EU Taxonomy tables

The tables below present the amounts within scope and the percentage of eligibility and alignment for each KPI related to the EU Taxonomy activities identified by PostNL. The table format has been updated according to the new one prescribed by Annex II of the Commission Delegated Regulation (EU) 2026/73 of 4 July 2025.

PostNL EU Taxonomy as indicated

For the year ended 31 December 2025

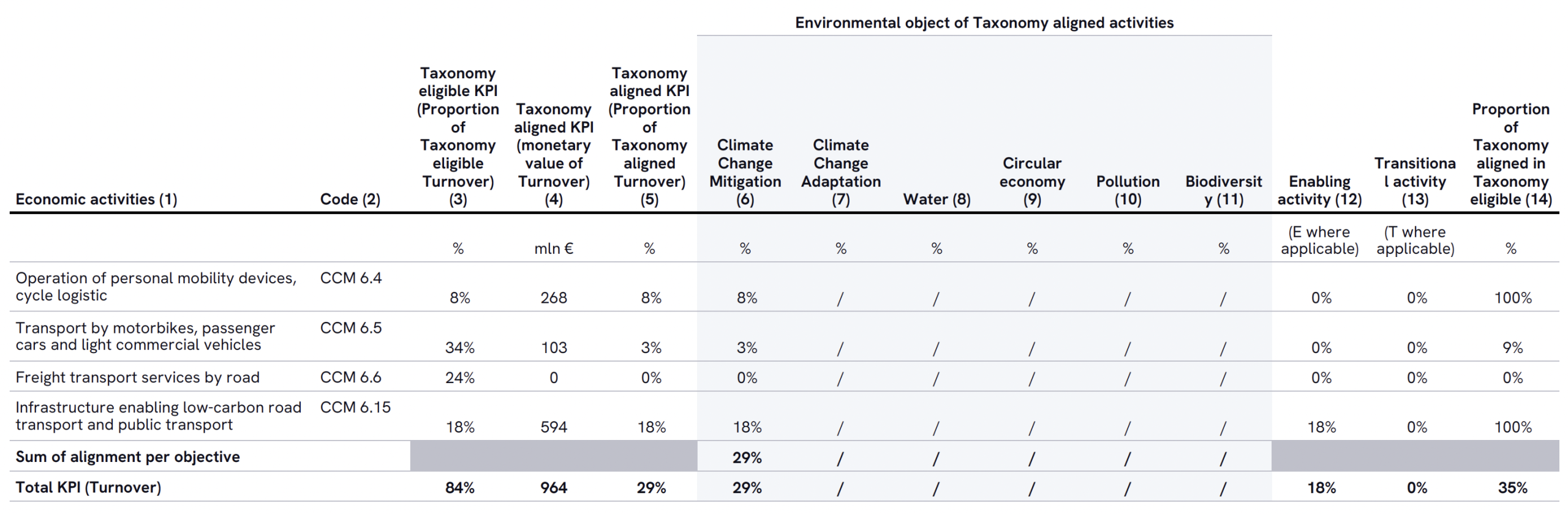

PostNL EU Taxonomy Turnover as indicated

For the year ended 31 December 2025

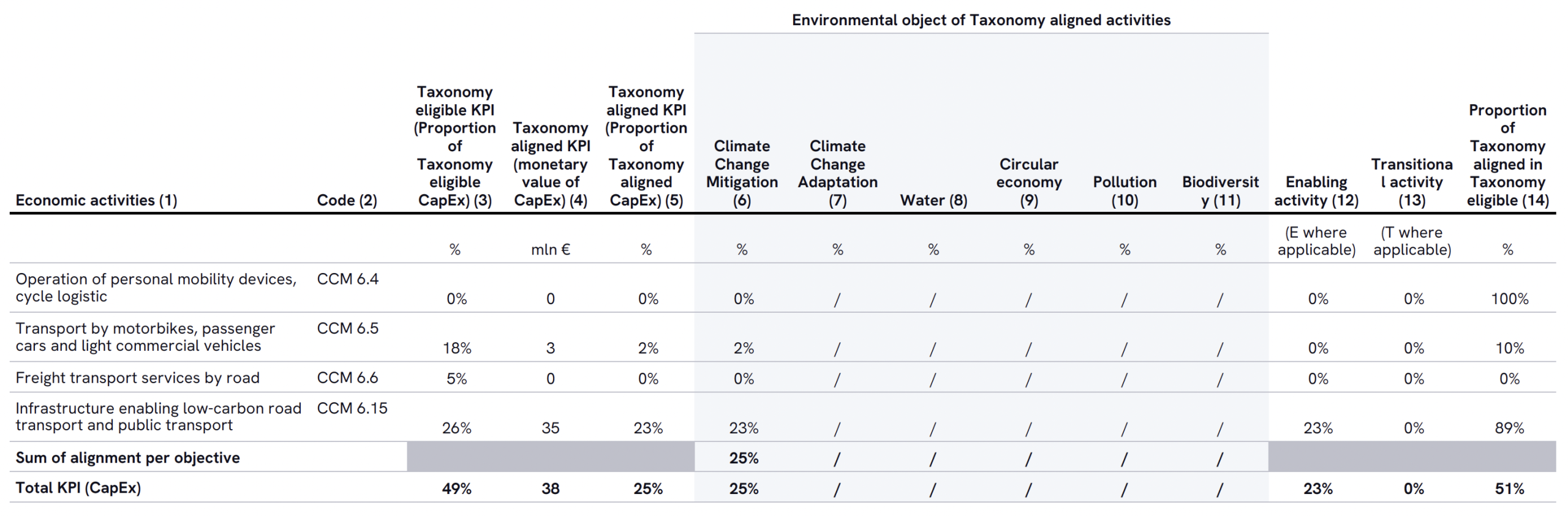

PostNL EU Taxonomy CapEx as indicated

For the year ended 31 December 2025

2.5.3 Performance

The EU Taxonomy prescribes quantitative and qualitative reporting on predefined KPIs. On the previous page we present the share of PostNL’s consolidated total revenue (turnover) and capital expenditure (capex) for the reporting period 2025.

Turnover

This KPI reflects the external revenue recognised in accordance with IAS 1 par. 82(a), and as such aligns with the ‘Total revenue’ reported in the consolidated income statement. To determine the portion of net turnover derived from Taxonomy-eligible activities for each revenue-generating stream, PostNL evaluated the extent to which these activities are encompassed by the EU Taxonomy framework.

The revenue deemed eligible under the EU Taxonomy primarily originates from activities related to the collection, sorting, and delivery of parcel and mail items. Accordingly, the eligible and aligned turnover under the EU Taxonomy pertains entirely to these logistics operations. Conversely, revenue not eligible under the EU Taxonomy is linked to the transportation of mail and parcels by air, services provided by external operators, and the coordination of logistics activities.

The allocation of revenue across various EU Taxonomy economic activities is determined based on the proportional operational costs associated with each activity. A detailed breakdown of turnover by EU Taxonomy activity can be found in the previous section. The EU taxonomy-aligned turnover 2025 is in line with prior years. The overall decline of 1 percentage point to 29% is mainly explained by a decrease in aligned turnover associated with the sorting and delivery process infrastructure (activity 6.15) for mail products.

Capital expenditures

This KPI covers the additions to Property, plant and equipment (PPE) under IAS 16, Intangible assets under IAS 38, as well as additions (including reassessments) to Right-of-use assets under IFRS 16 (see notes 3.2-3.4 to the Consolidated financial statements for more information).

From the total capital expenditures (capex), it is assessed which portion is Taxonomy eligible by assessing per asset category to which economic activity this asset category relates and to what extent this activity is included in the EU Taxonomy. The capital expenditures that are considered to be eligible under the EU Taxonomy include transport, infrastructure for transshipments (sorting activities) and real estate activities. The non-eligible capex under EU Taxonomy mainly relate to software and other equipment. The breakdown of the aligned capex for activity CCM 6.15 (Infrastructure enabling low-carbon road transport and public transport) shows expenditures for PPE of €31 million (2024: €26 million) and for RoU assets of €4 million (2024: €8 million). The increase in expenditure for PPE in 2025 is mainly explained by the expansion of automated parcel lockers (APLs) in the Netherlands as part of our out-of-home (OOH) strategy, and investments in tilters and other (un)loading and lifting tools as part of our focus on reducing physical strain in parcel sorting centres. The aligned capex for activity CCM 6.5 relates to lease contracts for electric scooters. The full table regarding the capex can be found in the previous section.

Operational expenditures

For operational expenditures (opex), where the operational expenditure is not material for the business model, the EU Taxonomy allows for an exemption (Article 8 Delegated Act Annex I section 1.1.3.2). PostNL is a people-driven and asset-light company. The denominator of the total opex in scope for the EU Taxonomy amounts to €66 million (2024: €64 million), which represents around 2% (2024: 2%) of PostNL's €3,324 million ‘Total operating expenses’ in 2025 (2024: €3,218 million). As PostNL applies an internally defined threshold of 5% (in line with previous year’s reporting), the relative share of opex in scope of the EU Taxonomy compared to the total operational expenditures of PostNL is deemed not material for PostNL's business model. As a consequence, the amount of eligible opex is exempt from the calculation of the numerator of the opex KPI for the EU Taxonomy and is therefore reported as being equal to zero.

Looking ahead

The current technical screening criteria offer limited scope for postal operators to achieve progress in alignment. In-depth analysis and discussions within a working group facilitated by PostEurop have demonstrated that meeting certain DNSH criteria is both practically and economically unfeasible. To address this, PostEurop, on behalf of its members, including PostNL, submitted a proposal to the European Commission for postal-specific economic activities and screening criteria. This proposal aims to establish criteria that are realistic and appropriate within the context of postal business models.

By introducing sector-specific criteria, European postal operators would be able to make meaningful investments in sustainable activities that align with their operational frameworks. Simultaneously, this would enable postal companies to achieve greater alignment in their EU Taxonomy reporting, fostering sustainable growth within the industry.