Our tax strategy and policy provisions

Introduction

PostNL’s tax strategy and policy are based on the mandate granted by the Board of Management to the Group Tax department. The strategy and policy set out the principles applicable across the PostNL Group and define and allocate roles and responsibilities in the area of taxation.

The objective of this tax strategy and policy is aligned with the Tax Governance Code (TGC) developed under the umbrella of VNO-NCW. This objective is to ensure a coherent, responsible and compliant approach to taxation in the broadest sense. Our conduct and approach to tax matters, as well as the related principles and procedures, are consistently aligned with this objective.

Tax strategy and risk management

Our approach to tax is fully aligned with PostNL’s overall strategy, whereby tax is viewed not solely as a cost factor, but as a contributor to socio-economic cohesion, sustainable growth and long-term prosperity. Accordingly, a coherent, responsible and compliant approach to taxation is considered an integral part of doing business, supported by a moderate tax risk appetite. Group Tax is mandated by the Board of Management to oversee this tax approach. In this role, Group Tax advises and supports the Board of Management on tax matters and acts as the central tax business partner for all stakeholders. Group Tax comprises specialists in direct and indirect taxes, payroll taxes, government grants, tax compliance and reporting.

Our approach to tax risk management is based on a tax control framework (TCF), which forms part of PostNL’s internal control framework. Key elements include periodic tax reports provided to the CFO, at least quarterly reviews of the tax position, and the execution of a quarterly tax risk management cycle, including (key) control execution and testing. In addition, Group Tax ensures adherence to the tax strategy and policies within the team and across the PostNL Group, thereby strengthening tax awareness. To support this approach, PostNL maintains ongoing dialogue with governmental and non-governmental stakeholders, industry groups and employer organisations on the interpretation of and compliance with tax laws and regulations.

Policy provisions

Approach to tax: tax strategy and tax policy provisions

We see tax not as a cost factor alone, but as a means for socio-economic cohesion, sustainable growth and long-term prosperity.

- Our approach to tax is based on a tax strategy and a set of policy provisions approved by our Board of Management

- Group Tax reports at least semi-annually to the Board of Management and at least annually to the Audit Committee on tax risks, adherence to the tax strategy and its underlying policy provisions

- Our tax strategy and its underlying policy provisions apply to all PostNL Group entities

- Our tax policy provisions apply to how we operate in our relationships with employees, customers, contractors and suppliers.

Accountability and tax governance

Tax is a core part of corporate social responsibility and governance and is overseen by our Board of Management.

- Our Board of Management is accountable for the tax strategy, the underlying policy provisions and tax risk management

- We have a tax control framework that sets out our tax controls and risk management

- Internal and external auditors regularly review tax controls as part of the audit of our financial results.

Tax compliance

We are committed to comply with the letter, the intent and the spirit of tax legislation in the countries in which we operate and to pay the right amount of tax at the right time.

- We prepare and file all tax returns required, providing complete, accurate and timely disclosures to all relevant tax authorities

- Our responsible tax planning is based on reasonable interpretations of applicable law and is aligned with the substance of the economic and commercial activity of our business

- We will not undertake transactions or engage in arrangements of which the sole purpose is to create a tax benefit that is in excess of a reasonable interpretation of relevant tax rules

- We will only claim tax incentives in line with the policy intent of such tax incentives and provided such incentives are generally available

- If we seek certainty in advance from tax authorities to confirm an applicable tax treatment, we do so based on full disclosure of all relevant facts and circumstances.

Business structure

We will only use business structures that are driven by commercial considerations, are aligned with business activities, and have genuine substance.

- We do not use so-called tax havens for tax avoidance. All entities in tax havens exist for substantive and commercial reasons

- We pay tax on profits according to where value is created within the normal course of commercial activity

- We use the arm’s length principle, in line with guidelines issued by the OECD, and apply this consistently across our businesses, contingent on local laws.

Relationships with tax authorities and other external stakeholders

Mutual respect, transparency and trust drive our relationships with tax authorities and other relevant external stakeholders.

- We seek to develop cooperative relationships with tax authorities, and relevant other authorities, based on mutual respect, transparency and trust

- We seek to engage constructively in national and international dialogue with governments, business groups and civil society to support the development of effective tax systems, legislation and administration

- We will work collaboratively with tax authorities to achieve early agreement on disputed issues and certainty on a real- time basis, wherever possible. Where there is controversy, we will strive to resolve the controversy by applying these principles.

Tax transparency and reporting

We regularly provide information to our stakeholders, including investors, policy makers, employees, civil society and the general public, about our approach to tax and taxes paid. We therefore publish the following information:

- A tax strategy or policy and our approach to tax risk management

- A list of group entities, with ownership information and a brief explanation of the type and geographic scope of activities

- Annual information on the corporate income tax we accrue and pay on a cash basis at a country level

- The total tax borne and collected by us, globally or per country, including corporate income taxes, property taxes, (non-creditable) VAT and other sales taxes, employer/ employee- related taxes, and other taxes that constitute costs to us or are remitted by us on behalf of customers or employees, by category of taxes

- Information on financially material tax incentives (e.g. tax holidays), including an outline of the incentive requirements and when it expires

- An outline of the advocacy approach we take on tax issues, the channels through which we engage in regard to policy development, and the overall purpose of its engagement.

Managing tax

Group Tax operates in line with recognised best practices in tax governance and compliance. It manages all relevant taxes and ensures the optimal use of available subsidy opportunities, in strict accordance with PostNL’s tax governance framework, strategy and principles. A key priority is promoting tax awareness across the organisation, supported by regular meetings and targeted communication initiatives. A cornerstone of PostNL’s tax governance is the tax control framework. The TCF is designed to identify, monitor and mitigate tax risks, while ensuring complete, accurate and timely tax reporting and compliance, and is fully embedded within the internal control environment. To maintain a robust and effective TCF, the Internal Audit department performs an annual audit of the TCF. When engaging third-party tax expertise, PostNL applies the principles set out in its tax governance framework and expects external advisors to adhere to these principles when providing tax-related services. Group Tax is responsible for identifying, assessing and managing the tax risks of PostNL. Identified tax risks and the effectiveness of the TCF are reviewed quarterly with the CFO.

PostNL has a moderate appetite for tax risk. Nevertheless, PostNL operates on a global basis and, as such, is potentially exposed to different types of risks, including those related to taxation. Examples of such tax risks that occur or have occurred for PostNL are:

- Adverse decisions or interpretations of tax authorities on pending disputes;

- Changes in tax treaties, tax laws, OECD Guidelines, EU Directives and other rules could have a material adverse effect on PostNL’s net result and cash flow; and

- Potential DTA impairments, due the fact that business results do not meet expectations or changes in applicable national and international (tax) legislation.

In 2025, PostNL participated for the third time in the peer review of the TGC initiated by VNO-NCW. In this process, PostNL acted both as a reviewer of another company’s compliance with the TGC and was subject to review itself. The outcome of the peer review was positive: the reviewer confirmed our assessment that PostNL was fully compliant with the TGC. PostNL will continue to participate in these monitoring initiatives.

Taxes in more details

An (inter)national trend is the increasing call for more transparency. PostNL assesses continuously its level of transparency in context of this trend. In 2025, the following developments and projects impacted PostNL’s tax position:

- The tax deductibility of liquidation losses arising from the winding-up of (former) Italian subsidiaries

- The carry-forward of tax losses

- Implementation of processes and controls regarding Pillar Two, as well as adhering to the first filing requirements.

- A goodwill impairment recognised in relation to Mail in the Netherlands

- A thorough review and update of our TCF

- The determination and implementation of tax and reporting implications of various treasury transactions.

- A new pension arrangement currently under discussion with the Dutch tax authorities.

The tax metrics (quantitative side of things) for 2025 will be expressed in more details in the next paragraph.

Total tax contribution

PostNL is transparent about its plans, activities, results and contributions to society. Tax follows the business and we consider our tax payments as a contribution to the communities in which we operate. PostNL’s total tax contribution (TTC) endorses our values in this matter: tax is paid in the country where we operate. As PostNL mainly operates from the Netherlands and Belgium, the TTC is predominately paid to the Dutch and Belgian tax authorities. Additionally, PostNL strives to be sustainable, which underpinned by the fact that we did not pay any material environmental taxes in 2025. For more information, we refer to the tables set out below.

PostNL General information in € million, unless indicated otherwise

Year ended at 31 December | 2024 | 2025 |

|---|---|---|

Number of employees (average FTE) | 20,151 | 19,398 |

Total revenue including interest | 3,275 | 3,343 |

Profit before income taxes | 25 | (18) |

Total income tax expense | 6 | 1 |

Effective income tax rate | 25.2% | (5.5)% |

The table below presents our total tax contribution for 2025. Given the different activities of PostNL, we pay a number of different taxes. In 2025, we paid €453 million in taxes (2024: €475 million). Below, we also present certain metrics per country.

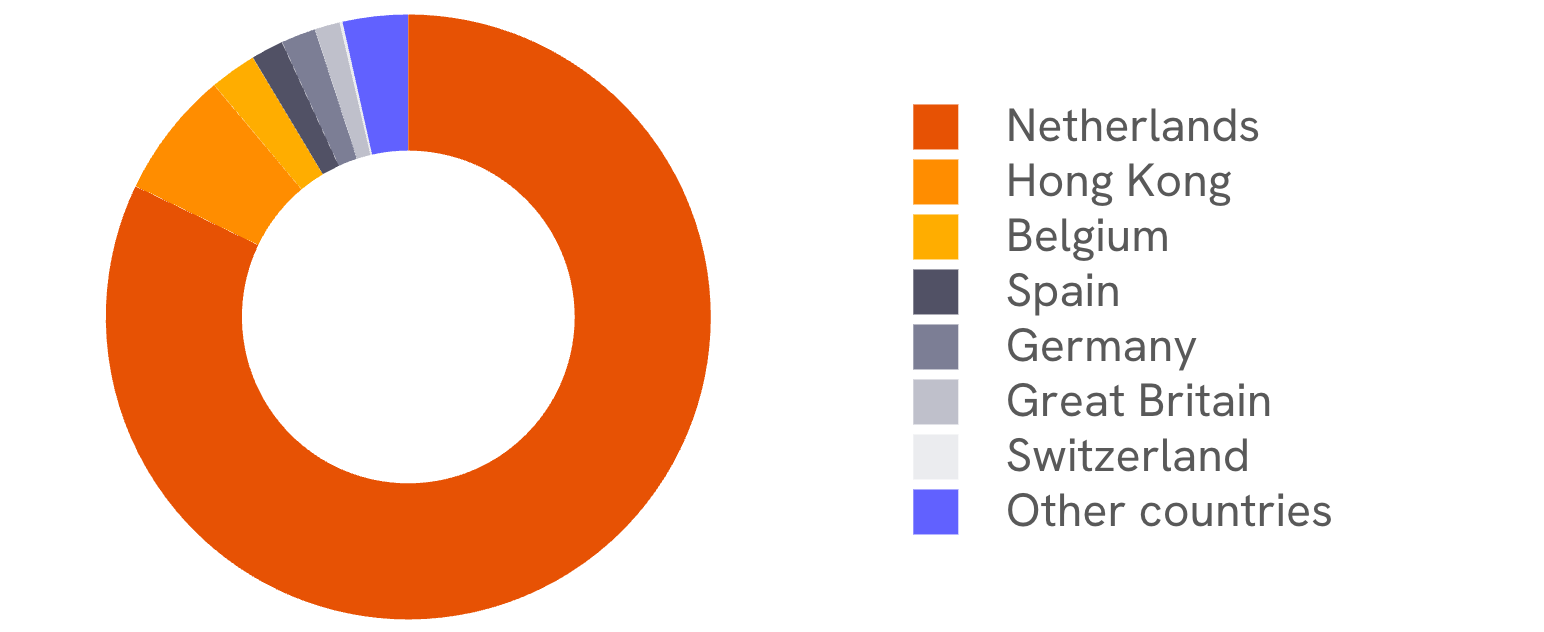

Total revenue including interest by country

2025: €3,343 million (2024: €3,275 million)

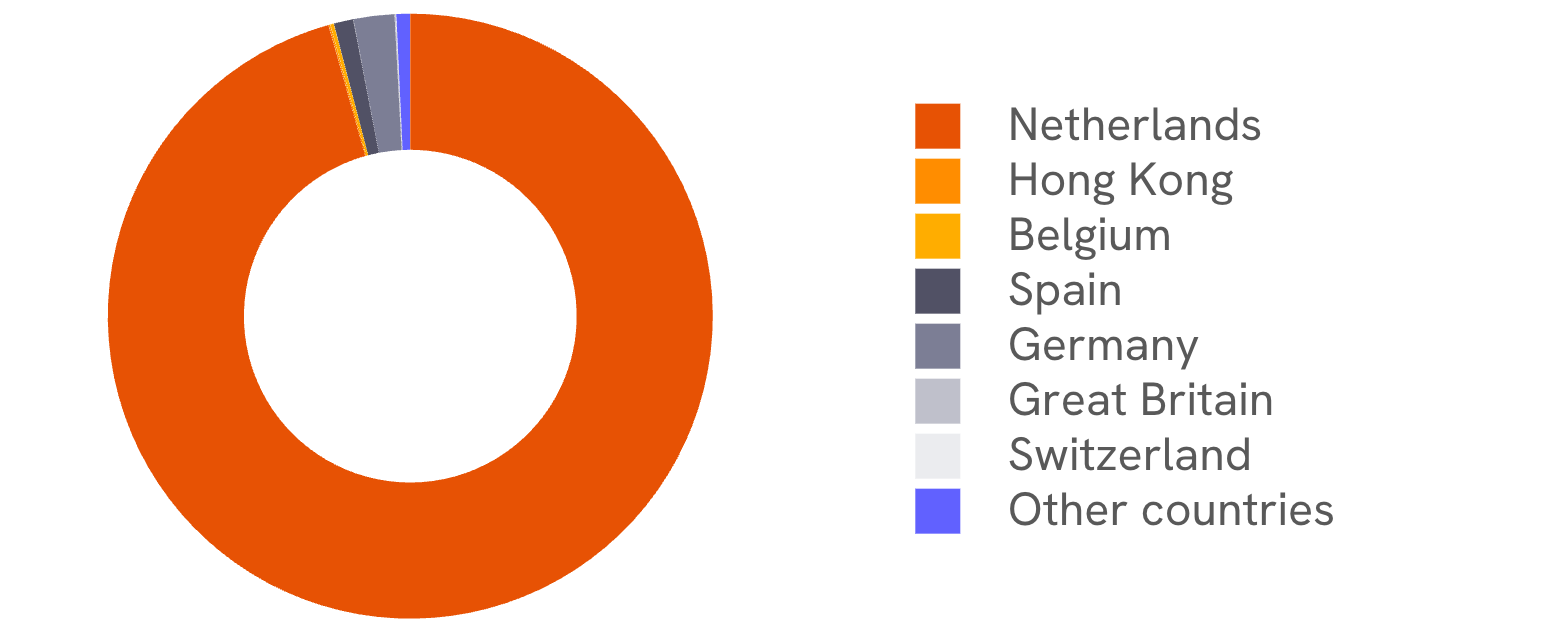

Taxes paid by country

2025: €453 million (2024: €475 million)

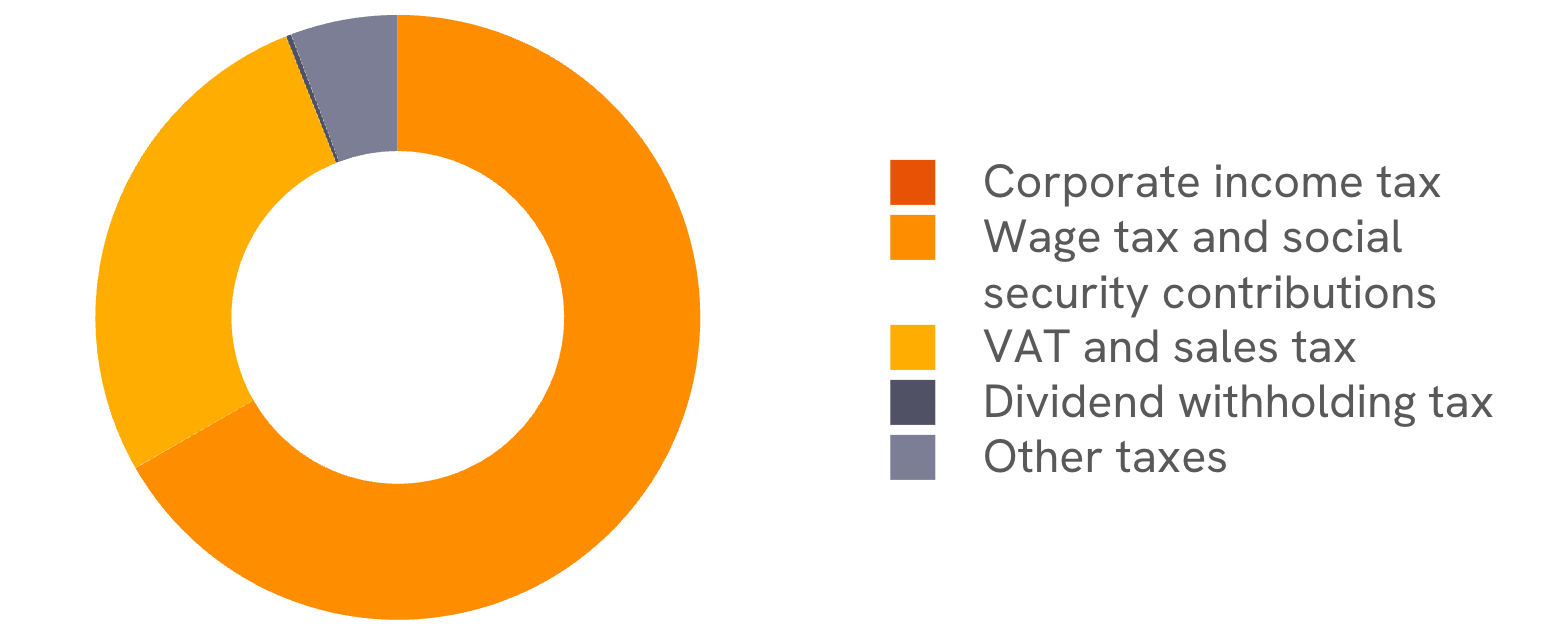

Taxes paid by type

2025: €453 million (2024: €475 million)

PostNL Taxes paid by type in € million

Year ended at 31 December | 2024 | 2025 |

|---|---|---|

Corporate income tax | 31 | (8) |

Wage tax and social security contributions | 296 | 307 |

VAT and sales tax | 128 | 126 |

Dividend withholding tax | 2 | 1 |

Other taxes | 19 | 26 |

Total | 475 | 453 |

The comparison between 2024 and 2025 indicates several changes in PostNL’s tax metrics. Corporate income tax differed from 2024, primarily as a result of the finalization of prior-year positions. Wage tax and social security contributions, VAT and sales tax, as well as other taxes, were broadly comparable to 2024.

Tax information per country

The vast majority of our business is currently concentrated in the Benelux. To provide transparency of our business, results and corresponding taxes on a per country basis, we provide a breakdown with general information and total tax contribution (borne and collected) as well as a list of group entities in appendix 4.

PostNL General information by country in € million, unless indicated otherwise

Country | Number of employees (average FTE) | Total revenue including interest | Profit/(loss) before income taxes | Total income tax expense | Effective income tax rate (in %) |

|---|---|---|---|---|---|

Netherlands | 18,288 | 2,745 | (24) | (1) | 2.5% |

Belgium | 630 | 84 | 5 | 2 | 38.5% |

France | 21 | 17 | 0 | 0 | (1.1)% |

Germany | 130 | 62 | 0 | 0 | (64.8)% |

Italy | 29 | 23 | 0 | 0 | 6.6% |

Great Britain | 72 | 45 | 0 | 0 | 25.2% |

Switzerland | 6 | 5 | 0 | 0 | 0.1% |

Spain | 99 | 58 | 0 | 0 | 52.0% |

Hungary | 12 | 2 | 0 | 0 | (20.3)% |

Czech Republic | 15 | 28 | 0 | 0 | 21.0% |

Poland | 11 | 7 | 0 | 0 | 13.2% |

United States | 21 | 8 | 1 | 0 | 27.9% |

Canada | 16 | 32 | 0 | 0 | (93.8)% |

Hong Kong | 46 | 227 | 0 | (1) | (180.8)% |

Singapore | 2 | 0 | 0 | 0 | 84.6% |

| Total 2025 | 19,398 | 3,343 | (18) | 1 | (5.5)% |

PostNL Total tax contribution (born & collected) in € million

Country | Corporate income tax | Wage tax and social security contributions | VAT and sales tax | Dividend withholding tax | Other taxes | Total tax contribution1 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

borne4 | collected | borne | collected | borne | collected | borne | collected | borne | collected | borne2 | collected3 | ||

Netherlands | 10 | 12 | 132 | (281) | 16 | (137) | 0 | (1) | 10 | (26) | 168 | (433) | |

Belgium | 2 | (2) | 12 | (19) | 0 | 21 | 0 | 0 | 1 | (1) | 14 | (1) | |

France | 0 | 0 | 0 | (1) | 0 | (2) | 0 | 0 | 0 | 0 | 0 | (2) | |

Germany | (0) | 0 | 1 | (3) | 0 | (7) | 0 | 0 | (0) | 0 | 1 | (10) | |

Italy | 0 | (0) | 0 | (0) | 0 | 2 | 0 | 0 | (0) | 0 | 0 | 1 | |

Great Britain | 0 | 0 | 0 | (1) | 0 | 1 | 0 | 0 | 0 | 0 | 1 | (0) | |

Switzerland | 0 | (0) | 0 | (0) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | (0) | |

Spain | 0 | (0) | 1 | (1) | 0 | (4) | 0 | 0 | 0 | 0 | 1 | (5) | |

Hungary | 0 | (0) | 0 | 0 | 1 | 0 | 0 | 0 | 0 | (0) | 1 | 0 | |

Czech Republic | 0 | 0 | 0 | (0) | 0 | (0) | 0 | 0 | 0 | (0) | 0 | (1) | |

Poland | 0 | (0) | 0 | (0) | 0 | (1) | 0 | 0 | (0) | (0) | 0 | (1) | |

United States | (0) | (1) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | (1) | |

Canada | 0 | (1) | 0 | 0 | 0 | 0 | 0 | 0 | (0) | 1 | (0) | (0) | |

Hong Kong | 0 | (0) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | (0) | |

Singapore | (0) | (0) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | (0) | (0) | |

| Total 2025 | 12 | 8 | 148 | (307) | 17 | (126) | 0 | (1) | 11 | (26) | 187 | (453) | |

| 1 | Zero amounts in this table are mainly the result of rounding in € million and therefore representing smaller amounts | ||||||||||||

| 2 | Taxes borne represent the taxes that are an expense/(income) item as included in the income statement. | ||||||||||||

| 3 | Taxes collected represent the taxes (paid)/received included in our cash flow, also representing payments made on behalf of other parties. | ||||||||||||

| 4 | The difference between the corporate income tax borne (€12 million) and the total income tax expense (€1 million) is due to changes in deferred taxes, see note 2.4.2 to the Consolidated financial statements. | ||||||||||||

| 5 | In 2025, there are no material allowances (such as the energy- and investment allowance in the Netherlands) and/or tax incentives applicable. | ||||||||||||